Welcome to JPE Brokers

Retirement Planning

Retirement Annuity

Preservation Fund

All Your Questions Answered

Request Callback

Saving for Retirement

It is very worrying if you look at recent statistics gathered by one of the bigger insurance companies in South Africa. The statistics indicate that a mere 6% of South Africans retire financially independent. The remaining 94% of South Africans are dependent on relatives, are forced to keep on working, or are dependent on the government. Your retirement planning strategy may include membership to a Pension or Provident Fund, discretionary investments, business interests and a property portfolio. Taking these strategies into consideration, if you have any non-pensionable income (even if only a portion of your income is non-pensionable eg. housing and/or car allowances etc, then a Retirement Annuity (R/A) is the most appropriate investment vehicle to use to supplement your retirement planning. Contribution to Retirement Annuities are fully tax-deductible up to certain limits, and is protected from creditors.

A Retirement Annuity is an investment vehicle designed to provide compulsory retirement proceeds to the individual policy holder or his/her direct dependents in a tax-efficient manner. The policy holder’s contributions are invested in the chosen investment fund portfolio, which are available at retirement age to purchase an annuity, which is payable to the policy holder on a monthly basis.

How does a Retirement Annuity Product work?

-

You make regular contributions towards a retirement annuity.

-

You receive a tax advantage – current legislation allows you to deduct a portion, or even all, of your contributions to a retirement annuity from your taxable income, subject to certain limits.

-

Your investment cannot be seized by your creditors. So your retirement savings are safe.

-

Your contributions are invested in investment funds of your choice, which grow over time through returns earned on the investment funds.

-

You can retire at any age from age 55.

-

When you retire, you will receive a retirement benefit.

-

Up to one third of your benefit can be taken in cash, while the rest must be reinvested, and used to pay you a regular monthly income or pension for the rest of your life.

Benefits of a Retirement Annuity:

There are many benefits associated with retirement annuities. The benefits you receive, for investing in a retirement annuity, are to encourage more people to provide for their retirement.

- The most important benefit of a Retirement Annuity is that it is a disciplined way of saving towards your retirement, and a Retirement Annuity is one of the most tax-efficient ways to save for retirement.

- There are many tax advantages associated with a Retirement Annuity:

Contributions are tax-deductible up to a certain maximum;

Disallowed contributions can be carried over to the next year of assessment and, if unused during the total contribution period, can be offset at retirement to increase the tax-free portion of the lump sum, the annuity or other income;

The funds you select within the retirement annuity are taxed very favourably (interest earned, dividend income and capital appreciation are tax free);

Your lump sum on death or retirement is tax-free up to R500,000;

Amounts more than R500,000 on death or retirement, enjoy a favourable tax rate;

You can deduct a further R1,800 per year, in respect of arrear retirement annuity contributions;

On death, any benefits paid out by way of an annuity are free of estate duty.

- Should you become insolvent, your money is safe in the retirement fund, as your creditors cannot seize the fund benefit.

- Should you change jobs, you do not have to terminate your investment, you simply continue contributing to the retirement fund.

- No executor’s fees are payable on retirement annuity benefits.

- Beneficiaries do not have to wait for the estate to be wound up before they have access to retirement annuity benefits.

- With the new generation retirement annuities, we offer a transparent savings vehicle with a variety of underlying investment options, so that you can spread your risk over time.

- You have a choice at retirement between a conventional annuity or an equity-linked living annuity.

- You can build up a fund for post-retirement medical expenses in a tax-efficient way.

Find a Retirement Annuity that will Work for You:

Every new generation retirement annuity product has its own unique characteristics regarding minimum and maximum payments available, funds to choose from, fees, loyalty bonuses, etc. Contact a JPE Broker who will assist you to find a new generation retirement annuity according to your unique needs and requirement.

A preservation fund is a fund in which employees, who leave the service of an employer owing to dismissal (including retrenchment) or resignation, or in the event of the dissolution of the employer’s pension or provident fund, may invest their accrued fund benefits.

The Income Tax Act also allows Membership to:

-

Persons to whom a pension interest from an ex-spouse’s retirement fund was awarded;

-

Employees of an employer whose business was taken over by another employer in terms of Section 197 of the Labour Relations Act, 1995;

-

Members of one preservation fund who choose to transfer to another preservation fund;

-

Members or dependents who do not claim their fund benefits from a pension or provident fund within 24 months of becoming entitled to it.

Why Choose a Preservation Fund?

Preservation funds have proved to be beneficial retirement vehicles for millions of people, because they enable people to preserve their existing retirement benefits until retirement. A person who wants to preserve retirement fund benefits in a preservation fund must be a member of the preservation fund. For many people, their disciplined preservation efforts pay off when they retire with an intact nest egg.

A preservation fund is an excellent investment instrument for tax-efficient savings, as preservation fund members receive two tax breaks:

- Monies in the retirement fund receive favourable tax treatment. Tax is not payable on rental income and interest, and no tax is payable on either capital gains or dividends received;

- The cash lump sum at retirement also receives favourable tax treatment. On retirement, a part of the lump sum could be tax-free, while the rest of the lump sum will be taxed at favourable rates.

Preservation Fund Features:

-

Money transferred from a provident fund to a preservation pension or provident fund, or from a pension fund to preservation pension fund, is currently tax-free. Refer to our Tax Guide for more information about tax-free transfers between funds;

-

A preservation fund is protected against creditors, which provides protection in the event of insolvency;

-

Any of the following compulsory annuities can be taken at retirement:

A conventional life annuity, with or without capital protection;

A linked annuity, which is more risky as a client has to choose underlying investment funds and percentage income;

A composite life annuity, which is a combination of a conventional life annuity and a linked annuity.

- The full benefit amount payable at death may be paid as a lump sum, or it can be used to provide regular income payments. The lump sum and income are subject to income tax, but exempt from estate duty;

- Depending on the transfer conditions, the full withdrawal benefit amount, or part of it, may be withdrawn as a lump sum from the fund once.

Contact a JPE Broker who will assist you to find the correctly aligned product for your unique circumstances.

At Retirement

When you have reached the important milestone of retirement, there are a few very important decisions to be made! It is critical to make the right investment choices that are aligned with your unique needs and circumstances. Some of the choices you make with compulsory monies (retirement fund money) are final, and can not be changed during your retirement.

Features of a Guaranteed Annuity:

- Guaranteed Annuities offer you an income for life in return for a single premium;

- You have the guarantee of a stream of future income for life, therefore never having to worry about running out of income during your lifetime;

- The insurer carries the investment risk of ensuring they have sufficient funds to pay you for the rest of your life;

- Life Annuity rates used mainly depend on two factors:

Effect of Interest Rates:

The higher the long-term interest rates when you purchase the annuity, the higher the income amount and vice-versa.

Effect of Period of Payment:

The shorter the expected period of payment, the bigger the income, and vice versa;

Life expectancy differs for males and females;

Factors which entail a longer expected period of payment, such as a guarantee term or survivor’s income, will mean a lower monthly income.

Guaranteed Annuity Types:

The type of annuity you select will determine the income you will receive. An annuity, on the life of one person without any minimum guaranteed payment term and without any yearly growth in annuity income, will secure the largest annuity income. If you buy the annuity on more than one life, add guaranteed minimum terms or increase your yearly annuity income, the product provider’s risks increases, and the annuity income will be adjusted downwards. The choices you have to make when you buy a guaranteed annuity are:

Single-Life or Joint-Life Annuity Option:

You can receive an annuity calculated on your life alone, or you can choose to receive this annuity calculated as part of a joint-life annuity. This form of annuity provides income to your spouse or children upon your death, and therefore also provides a form of death benefit, but paid in regular amounts. This helps manage your dependent life risk.

Guaranteed Term Annuity Option:

You can choose to receive this annuity for a fixed minimum period, irrespective of whether you survive that period. This therefore allows income to be generated for a minimum period to benefit your family if something happens to you before this minimum period expires. When you survive this minimum period, the payment is then made to you for the rest of your life. Again, this feature gives you an added control of your dependant life risk.

The above features show the benefits of managing long life risk, and also to provide a protection benefit to your family members. However, another important issue that comes up with this product is the form of the payment that you want to receive for the rest of your life. These can currently come in four forms:

Level Annuity:

You will receive a fixed and level payment for the rest of your life. This is the cheapest form of annuity product because there are no changes to your payment stream, and it is guaranteed for the remainder of your life. This form does not give you protection from inflation risk because, over time, the prices of goods and services increase but your income remains constant.

Fixed Increases Annuity:

You shall receive payments which increase annually at a fixed percentage chosen by you at the start. This form of annuity allows you to choose the percentage at which your payments can increase, and therefore allows you some inflation protection. You will encounter inflation risk, if the rate of inflation is higher than the fixed increase that you chose at the start.

Inflation-Linked Annuity:

You will receive payments which increase annually at the rate of inflation in the economy. This therefore reduces inflation risk considerably. Most annuities of this type offer a minimum increase of 0%, so your annuity will not decrease if deflation occurs.

Discretionary Growth Annuity:

You will receive a guaranteed minimum payment that increases annually, at a growth rate decided by the insurer. This growth rate is based on returns earned by investing your single premium, in attempting to offer you growth in your income each year. You still face inflation risk if the growth declared by the insurer on your income is less than the rate of inflation applicable at that time. Your growth is also dependent on the underlying assets that are used to generate this growth on your income.

Summary of Guaranteed Annuity:

In summary, guaranteed annuities offer you an income (in various forms) for the rest of your life (or your spouse’s/children’s lives) for a possible minimum guaranteed period. It allows you to control your long life risk and inflation risk, as well as providing protection benefits for your family upon your death. The main disadvantages of this product are that there is very little flexibility when it comes to the income that you want to receive after you have purchased this product because, as your circumstances change, you cannot change your benefits, and in a low interest rate period, your annuity will buy a smaller income (pension) than buying it in a higher interest rate period. Another important restriction on this product is that you are not allowed to surrender your policy unless you provide proof of transferring to another insurer, or provide proof of good health to the insurer.

Why Invest in an ILLA?

A regular income from a flexible retirement investment product:

You can vary your income level and the frequency at which you receive your income each year, thus enabling you to match your cash flow to changing needs.

Control of your underlying investment, tailored to your specific risk profile:

You can choose from a range of more than 900 funds managed by leading asset managers. Select appropriate funds to tailor your investment choices to meet your own individual risk profile and needs. An experienced and qualified stockbroker can manage your portfolio on your behalf.

To leave a legacy to your dependents if you pass away:

At death, the money available in the living annuity is not forfeited, but can be transferred to the policyholder’s nominated beneficiaries. The beneficiaries may continue with the income payments, or receive a once-off payment.

A tax efficient retirement solution:

No tax is payable on your investment returns and capital gains. You only pay tax when you receive the income.

Considerations when Investing in an Investment-Linked Living Annuity:

The main factors that influence the income of an Investment-Linked Living Annuity (ILLA) are:

- The income level selected, together with current and future rates of inflation;

- The performance of the selected underlying investments, which depends partly on the asset allocation; and

- The lifespan of the annuitant (how long you live for – if you live longer than the initial estimate, this exposes you to longevity risk).

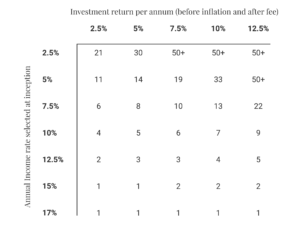

Effects of Income Level and Investment Return on Sustainability:

The Association for Savings and Investments SA (ASISA) has provided a table that serves as a guide to the sustainability of a specific level of income, for a given level of investment return in the portfolio after fees are deducted. However, markets and circumstances change, and it is therefore vital that you, together with an intermediary, review your income withdrawal percentages on an annual basis.

The table below shows the number of years it will take before your income starts to reduce, given a specific investment return in your portfolio and a selected annual income rate. The table assumes that your income will be adjusted annually to allow for inflation, i.e. to maintain your standard of living.

Number of years before your income starts to reduce in today’s monetary terms, i.e. after taking into account inflation of 6% per annum.

The number of years that your ILLA will last, increase or decrease according to:

- the investment return of the portfolio (shown in the table above); the investment return is dependent on the asset allocation of your portfolio, your selection of funds and the fees charged in the portfolio; and

- your chosen income percentage (shown in the table above).

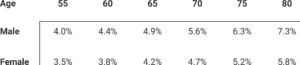

Selecting an Appropriate Income Level for Your Age:

As a further guideline, a major insurance company in South Africa has compiled a table which gives guidelines to help you in selecting an appropriate level of income for your age. You should note that the percentages in the table give an indication of the maximum percentages that should be withdrawn after fees are deducted. The levels are set to target an income that should not reduce in real terms (in other words, after taking inflation into account) during your lifetime, and which will not exceed the regulatory maximum income rate.

You should compare your current age to that in the table. Depending on your individual circumstances, it may be prudent to draw a lower amount. You should consult with your financial planner before investing in an ILLA, and even more so if the ILLA is your only income and you require a pre-tax income that exceeds the level indicated in the table. If you are already invested in an ILLA, you should also consult with your financial planner if your portfolio is generating a real return of less than 2 % after fees, and you require an income that exceeds the level in the table.

The insurance company gives the following guidelines for the maximum level of income for your age. These guidelines are based on a portfolio that generates a real return of 2% per annum after fees are taken into account. Where a lower real return is generated, a lower income level should be considered. Use the cash-flow calculator to see the effect of % income on the term.

One of the bigger insurance company’s guidelines on maximum withdrawal levels:

Legislation allows you to draw an income of between 2.5% and 17.5% of the capital value of your ILLA investment.

It is essential to choose an appropriate income level for your age. If you choose an income level that is too high, your capital value will not be sustained. In other words, your income will not increase and may even decrease with time. This means that you will have less purchasing power, and you will not be able to maintain the same standard of living.

Choosing an Appropriate Asset Allocation:

It is important to find your tolerance towards risk. Although there are no specific limits prescribed by legislation for living annuities, the Association for Savings and Investment South Africa (ASISA) provides guidance on what may be considered prudent investment limitations:

- No more than 75% should be invested in equities;

- No more than 25% should be invested in property;

- No more than 25% should be invested in foreign assets.

Longevity Risk:

Longevity Risk is perhaps the biggest risk to investment-Linked Living Annuities. In general, people are living longer today than previously. In retirement planning, you generally assume an age until which you require income. It is critical that you also evaluate the likely impact on your future income should you live longer than originally assumed, as longevity risk within an ILLA is borne solely by you.

Tax and Fees:

Tax

The investments within an ILLA are not subject to income or capital gains tax. Only the annuity income is taxed in your hands, and it is subject to individual tax rates.

Fees

Product Provider

- Administration fees (no administration fees for switching between underlying funds).

Other

- Asset management fees for managing and trading the investments;

- Financial intermediary fees (negotiable with intermediary).

A full break down of fees and charges will be given when you request a quote from your financial adviser.

Transfers:

You may transfer the ILLA to a conventional annuity. Transfers are done at current market value, with the provision that the relevant regulatory requirements are met.

Review Each Year:

Note that markets and circumstances change. It is vital that you review your income level each year. You may be able to reduce the risk related to investing in an ILLA, by:

- investing part of your capital in a Conventional Life Annuity, or

- selecting the underlying investment options that are most appropriate to manage your investment risk. Linked product companies offer a wide range of investment choices, including collective investment funds, shares and fixed instruments.

What is a Retirement Annuity?

A retirement annuity is the policy which is selected by a member or prospective member of a retirement annuity fund, and taken out by the retirement annuity fund, to accumulate the capital to provide the member with an annuity at retirement. The member’s contributions to the retirement annuity fund are used as contributions for the policy.

How is a Retirement Annuity Structured?

A retirement annuity is structured to provide you with a pay-out at any age from your 55th birthday. Legally, up to one third may be taken in cash. The rest must be reinvested, and the proceeds used to pay you a regular monthly pension for life.

What are the Advantages of Retirement Annuities?

While there may be factors that could threaten your retirement provision, such as not being able to save enough, debt, inflation, essential household and nursing services, and medical expenses, a retirement annuity provides you with one of the best retirement provision instruments available. You can put it to work in different ways – as a disciplined way of saving, or to top up your existing retirement fund. You can also make use of the tax concessions it provides.

What will Your Contributions be?

The affordable contributions start from a minimum of R200 per month for an investment term of 15 years or longer. The minimum contribution will however be determined by the product provider you select, and the term of your retirement annuity. To boost your investment, you can inject extra lump sums at any time, and also increase the contribution by between 2.5% and 20% every year, to counteract the eroding effects of inflation.

What are the Investment Options in the Retirement Annuity?

The Retirement Annuity offers you a comprehensive range of investment funds – from funds that fluctuate in accordance with the stock market, to investment funds with optional guarantees that offer more security. You can choose to invest in one fund, or spread your contribution among a combination of funds. The first step, however, is to determine the level of risk you are willing to take with your retirement savings, whether you are looking for a high-, medium- or low-risk investment, or a combination of all three. You also have the option when you request a quotation, or apply for a retirement annuity, to instruct us to suggest funds that are aligned with your risk profile and savings objective.

What are the Tax Benefits of a Retirement Annuity?

- Contributions are tax-deductible up to a certain maximum;

- Disallowed contributions can be carried over to the next year of assessment and, if unused during the total contribution period, can be offset at retirement to increase the tax-free portion of the lump sum, the annuity or other income;

- The funds you select within the retirement annuity are taxed very favourably (interest earned, dividend income and capital appreciation are tax free);

- Your lump sum, on death or retirement, is tax-free up to R500,000;

- Amounts more than R500,000, on death or retirement, enjoy a favourable tax-rate;

- You can deduct a further R1,800 per year in respect of arrear retirement annuity contributions;

- On death, any benefits paid out by way of an annuity are free of estate duty;

- If you leave your employer and receive a withdrawal benefit from your pension or provident fund, you can preserve your retirement benefit, transferring it into a Retirement Annuity fund tax-free.

What is Pensionable and Non-Pensionable Income?

Pensionable income is the income used by your employer to calculate your pension or provident fund contribution. This income will typically include any fixed remuneration (e.g. salary or wages), but may exclude variable amounts, such as commissions, bonuses and overtime. Non-pensionable income is your taxable income, excluding (if any) your pensionable income, retirement fund lump sum benefits, assessed losses and capital gains.

What is the Maximum Tax-Deductible Contributions to Retirement Annuities?

The maximum deductible current contributions to Retirement Annuity fund(s), made during a year of assessment by a “natural person”, is:

- 27.5% of gross taxable income (R350,000 p.a. maximum for all reirement investments).

How Many Retirement Annuities Can You Take Out?

You can invest in as many retirement annuities as you wish, but the tax benefit is determined in aggregate, not in respect of each individual retirement annuity. The tax relief on contributions is limited to the formula discussed above, and the tax-free lump sum portion may be claimed only once.

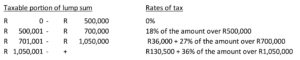

How Are Retirement Annuity Retirement Lump Sum Benefits Taxed?

The taxable lump sum cannot be set-off against any of your assessed losses.

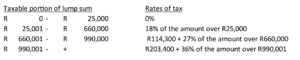

How Are Retirement Funds Withdrawal Lump Sum Benefits Taxed?

The taxable lump sum cannot be set-off against any of your assessed losses.

What Happens to the Retirement Annuity if I Pass Away?

Should the worst happen, and you pass away, the value of the investment is available to your appointed beneficiaries and/or dependents. No executor’s fees are payable, and your beneficiaries do not have to wait for the estate to be wound up before they have access to the money. In line with section 37 of the Pension Funds Act, the trustees of the retirement fund will distribute the proceeds, considering first the needs of your dependents, and then the beneficiaries listed in your nomination form. It is thus important to keep your nomination up to date. Your investment will be taxed on the same basis as on retirement. Can you stop contributing to your retirement annuity? Yes. You can make your Retirement Annuity “paid-up”. This means you no longer pay monthly contributions, however, you will stay invested until you retire. You may retire from age 55 onward.

Can My Employer Contribute to a Retirement Annuity on My Behalf?

Yes, your employer can contribute towards a retirement annuity on your behalf. Where an employer pays the retirement annuity fund contribution on behalf of its employee (member), it is a taxable benefit for the employee, but also with a deduction for the employee within limits. The payment on behalf of the employee is a deductible expense for the employer.

May a Part of My Accumulated Credit in my Retirement Annuity be Paid to My Former Spouse on Divorce?

Your accumulated benefit will only be affected, if the Settlement Agreement made provision for the allocation of a portion of the ‘pension interest’ in the Fund to your former spouse, and this is made an order of the court. The Divorce Act and Pension Funds Act have specific requirements which must be met before the Fund has to make payment of any portion of your accumulated benefits to your former spouse. If you are contemplating divorce, and are considering allocating a portion of your accumulated credit to your spouse, please consult with a financial adviser and an attorney, who are familiar with the relevant legislation, and who will be able to highlight the potential pitfalls, and ensure that all the requirements are met. If the requirements are not met, the Fund will not be able to make any such payment.

Who Pays the Tax when I Allocate a Portion of My Benefits to My Spouse on Divorce?

National Treasury issued a Media Statement on 13 March 2012 advising that it intends amending the taxation of divorce orders that are paid by retirement funds on/after 1 March 2012. And the South African Revenue Services (SARS), which is responsible for the calculation and collection of taxes, has confirmed that administrators must now process the taxation of divorce orders, in terms of this Media Statement. Therefore, for divorce orders paid on/after 1 March 2012, irrespective of whether they are paid from an occupational fund, retirement annuity fund or public sector fund, will be paid as follows:

Divorce Orders Issued: Pre-13 September 2007

- Non-member spouse makes election on or after 1 March 2009, but before the member’s exit from the fund – un-taxed;

- Non-member spouse makes election on or after 1 March 2009, but after the member’s exit from the fund – un-taxed.

Post 13 September 2007 Divorce Orders

- Non-member spouse makes election on or after 1 March 2009, but before the member’s exit from the fund – taxed (non-member spouse is taxpayer);

- Non-member spouse makes election on or after 1 March 2009, but after the member’s exit from the fund – taxed (non-member spouse is taxpayer).

Can I get Access to My Benefits in the Fund if I Emigrate from RSA?

The Income Tax Act has been amended to allow a member who has not yet retired, but who has ceased the payment of contributions towards an annuity contract and has emigrated, to receive upon written request the cash value of his retirement annuity contract, subject to tax. This applies irrespective of the value of the investment. Such payment is, however, subject to the requirement that the member’s emigration is recognised by the South African Reserve Bank.

What are the Duties of the Board of Trustees when a Member of a Retirement Annuity Fund Passes Away?

In terms of Section 37C of the Pension Funds Act 24 of 1956 (as amended), and the Rules of Retirement Annuities one of the important duties of the Board of Trustees of the Fund, is the distribution of death benefits upon the death of a member. In terms of the above, the Trustees are required to:

- Identify and trace dependants and nominated beneficiaries of the deceased member of the Fund;

- Establish and investigate each dependant and nominee’s circumstances;

- Allocate death benefits on a fair and equitable basis at the sole discretion of the Trustees.

Who Qualifies for Consideration for Benefits by the Trustees when a Member Passes Away?

Dependants are defined according to specific criteria in the Pension Funds Act 24 of 1956 (as amended), and may either be legal or factual dependants, including:

- The surviving spouse of the deceased member;

- All of the deceased member’s minor and major children (whether they are biological, legally adopted or born out of wedlock);

- Anyone proven to be factually dependent on the deceased for maintenance; and

- Anyone, to whom the deceased member was legally liable for maintenance, or would have become legally liable for maintenance, had the member not passed away.

Should I Update the Beneficiary Nomination on My Retirement Annuity?

Where there are dependants at date of death, nominees can only be considered for participation in benefits if they were nominated on or after 30 June 1989. Due to a change in legislation on 30 June 1989, earlier nominations can only be considered if no dependants exist at date of death. A beneficiary nomination is an indication of the member’s wishes, and it must be noted that such nomination will not be binding on the Trustees of the Fund. Unlike a life policy, the nominee does not obtain a right to receive the death benefits (or part thereof) in terms of the nomination. Nominated beneficiaries who were nominated on or after 30 June 1989, will be considered along with other qualifying dependants. The general purpose of a retirement annuity is to provide for the member’s dependants, in the event of the member’s death. As members’ circumstances may change from time to time, it is of the utmost importance to nominate a beneficiary(ies), and to keep any nomination up to date.

Can I Nominate My Estate as Beneficiary on My Retirement Annuity?

Please note that your estate cannot be nominated as a beneficiary on a retirement annuity. It should also be noted that the death benefits of a retirement annuity do not form part of the assets of a deceased member’s estate, and can thus not be bequeathed by will, nor can it be ceded.

Can I Nominate a Trust or Charitable Organisation as Beneficiary on My Retirement Annuity?

A trust, a company or charitable organisation may not be nominated to receive the benefit, as the Trustees of the Fund are obliged to determine and confer benefits upon dependants in terms of the Pension Funds Act 24 of 1956 (as amended). These entities do not qualify as dependants.

What is Regulation 28 that My Retirement Annuity Funds Must Comply to?

- The Retirement Annuity Fund is governed by the Pension Funds Act;

- Regulation 28 requires that all new retirement contracts meet the requirements;

- Regulation 28 aims to protect you. It therefore limits the maximum allowed for each asset class, to make sure that your contributions are invested wisely;

- Amongst other stipulations, Regulation 28 prescribes the maximum exposure that retirement fund investments may have, to various asset classes, as follows:

75% in equities

25% in property

25% in offshore assets

Is the Tax Deduction You Receive on a Retirement Annuity Contribution Really Any Good?

We will demonstrate by means of an example, what effect the tax deduction you receive on a contribution towards a retirement annuity can have.

Assume

- A deduction of R500 pm (R6,000 per year) are allowed;

- Your marginal tax rate is 26% (Earning between R195,851 – R305,850 pa – Tax Year 2019/2020).

If you do not contribute the above mentioned R6,000 towards a retirement annuity, you will have R4,440 (after tax) to spend or save in another product.

If you decide to invest in a retirement annuity instead of spending or saving the money (after tax) in another product as mentioned above, you are saving R4,440 plus the subsidy of R1,560 (the tax you would have paid), which adds up to R6,000. This constitutes an immediate return of 35% for the year on your savings (R1,560 on the R4,440), before you have even earned a cent in the investment fund! *

* If your marginal tax rate is 41% (Earning more than R708,311 – Tax Year 2019/2020), you would have been subsidised by R2,460 on a payment of R6,000, which constitutes a return of 69%!

A return of 35% pa, AND that is not where it ends!

The fund you invest in within the retirement annuity vehicle, is taxed at very favourable terms (interest earned, dividend income and capital appreciation are tax free). This means that if you do not spend the after taxed money, and decide to invest in a product other than a retirement annuity, the return would be less than received on a retirement annuity, because of the taxation of the benefits received within the investment vehicle!

Summary

In the above-mentioned example, you receive 35% return on your money in only one year, before you have earned a cent in the investment funds you select!

Your investment return is more in a retirement annuity, if you compare the investment fund with a similar fund that is structured for voluntary (after taxed) monies.

A retirement annuity is an excellent savings vehicle for retirement. Contact Us for an Appointment with a Financial Adviser.

Send us a message

To apply for access to a record, kindly complete Form 2 and email it to admin@jpebrokers.co.za.

Once we have reviewed your request, JPE Brokers will provide you with Form 3, confirming the outcome of your application as well as any fees that may be payable.